For Benefits Brokers & Consultants

Help your self-funded clients cut high-cost surgical claims by 50–70%. Give their employees $0 out-of-pocket access to comprehensive care — and build the kind of renewal story that protects your book.

Download the broker partnership overview — Broker Partnership Overview

See what your client's plan could save — Savings Estimate Form

Contact us to schedule a discovery meeting today!

Contact Us to Add Aptiva to Your Book

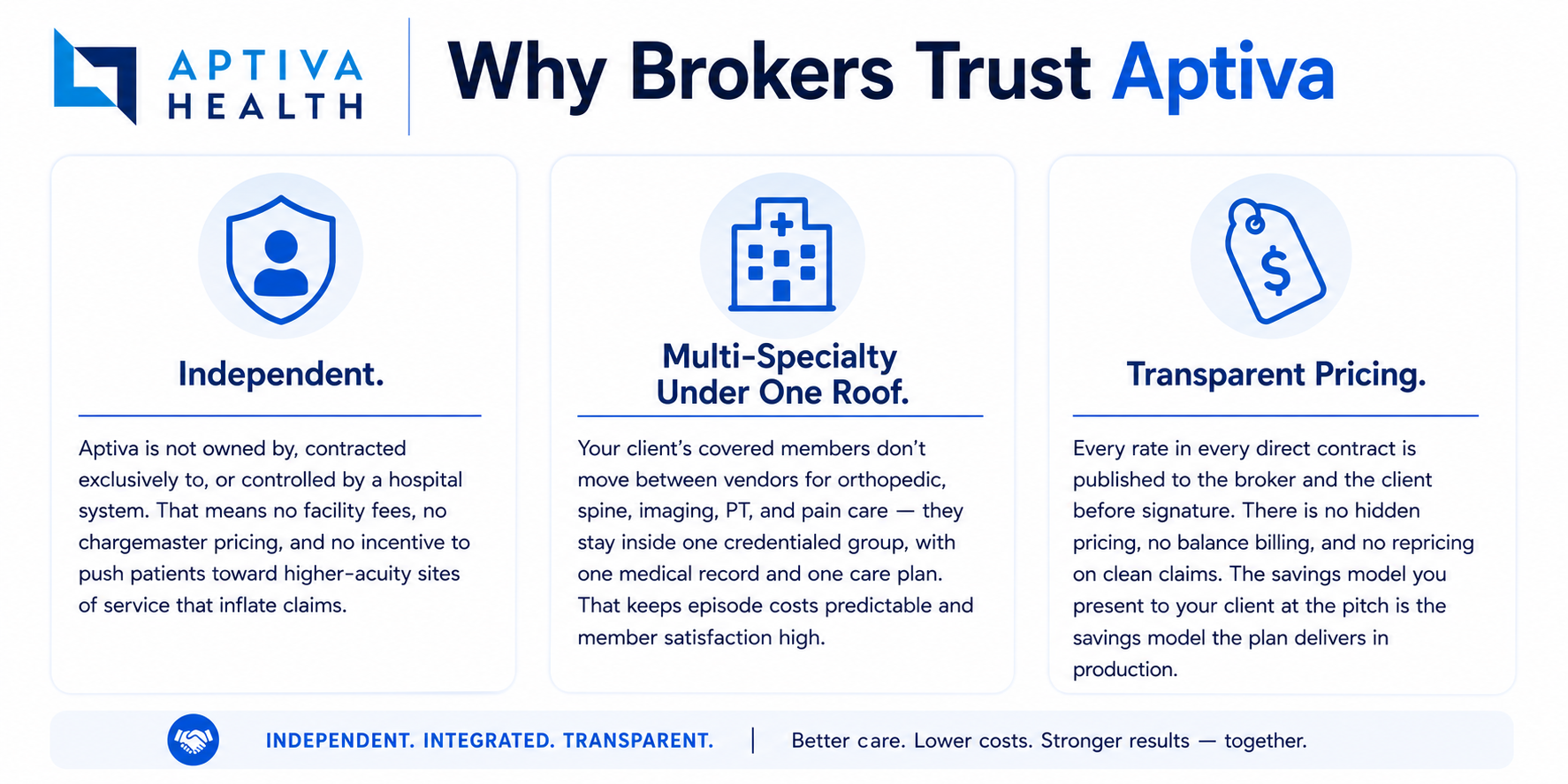

Your Clients' Highest-Cost Claims Are Also Your Biggest Renewal Risk

Orthopedic and spine procedures are some of the most expensive and most unpredictable claims for self-funded plans — and they're also the line items competing brokers point to when they're pitching against your renewal. Hospital-based facility fees, surprise bills, separate charges from surgeon, anesthesia, and facility, and aggressive chargemaster pricing combine to produce six-figure claim variability that no actuary can model cleanly. That variability is what makes plans hard to defend at renewal.

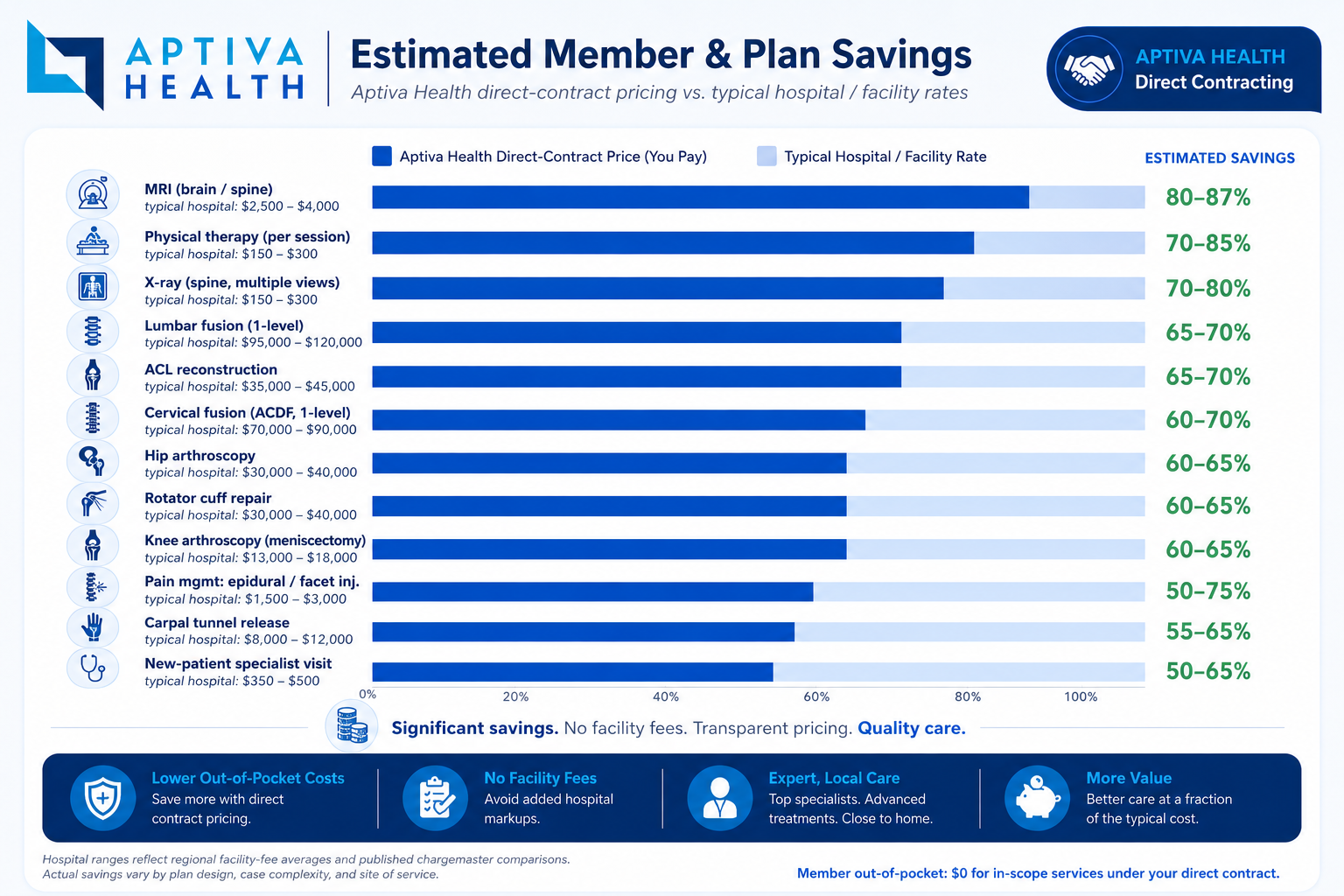

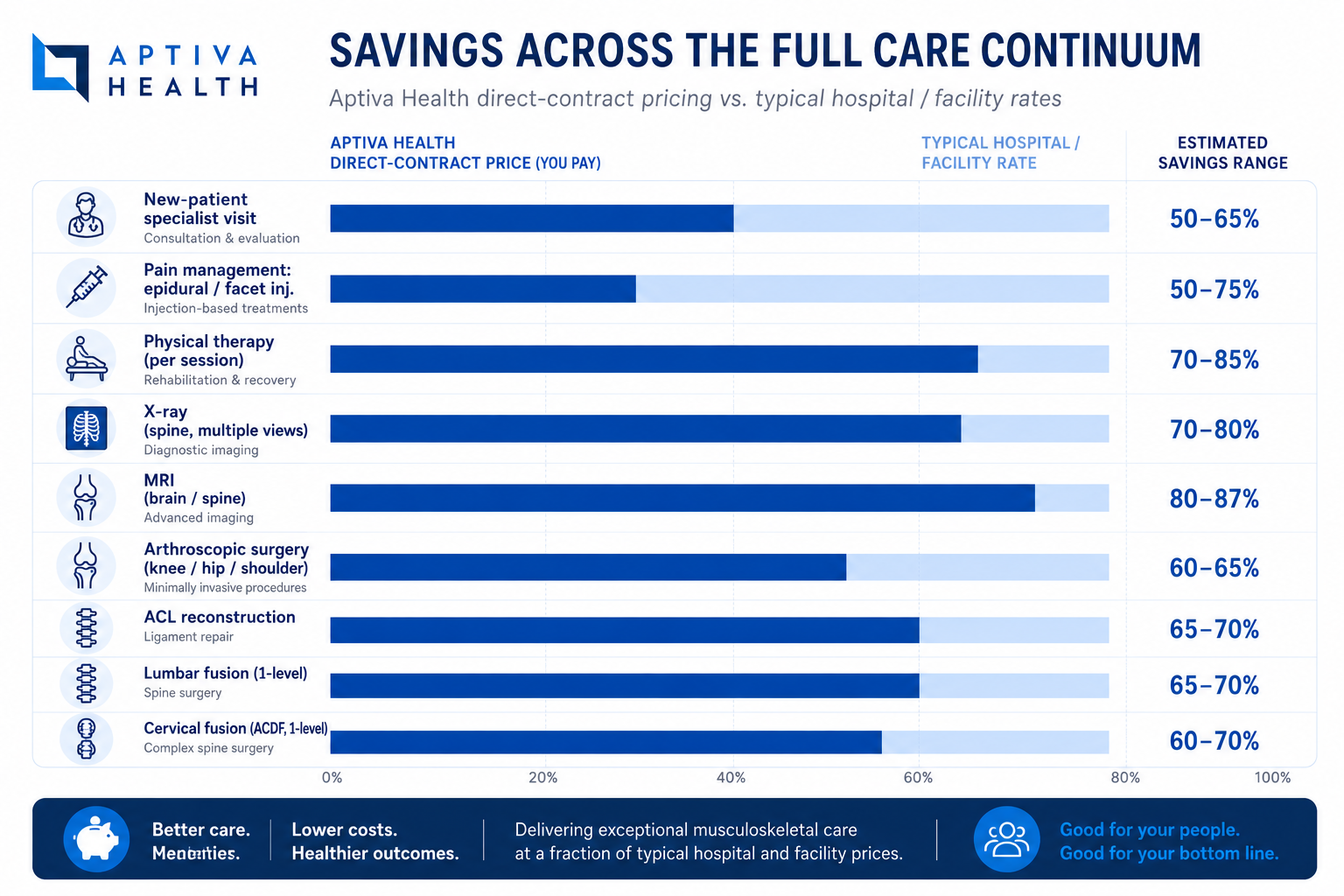

A direct contract fixes the variability at its source: one bundled rate, negotiated directly with your client's plan, all-inclusive, paid in full without repricing. The savings show up on the claims report your client sees mid-year, and they become the centerpiece of your renewal presentation. The chart below shows the kind of savings our current employer partners typically see — your client's actual rate schedule is built specifically for their group.

What Direct Contracting Typically Saves a Client Plan

Hospital ranges reflect regional facility-fee averages and published chargemaster comparisons. Savings ranges shown are illustrative of outcomes seen across our current direct-contract partners; your client's actual savings will depend on the negotiated rate schedule, plan design, and case mix. Each Aptiva direct contract is custom-built for the employer plan it covers.

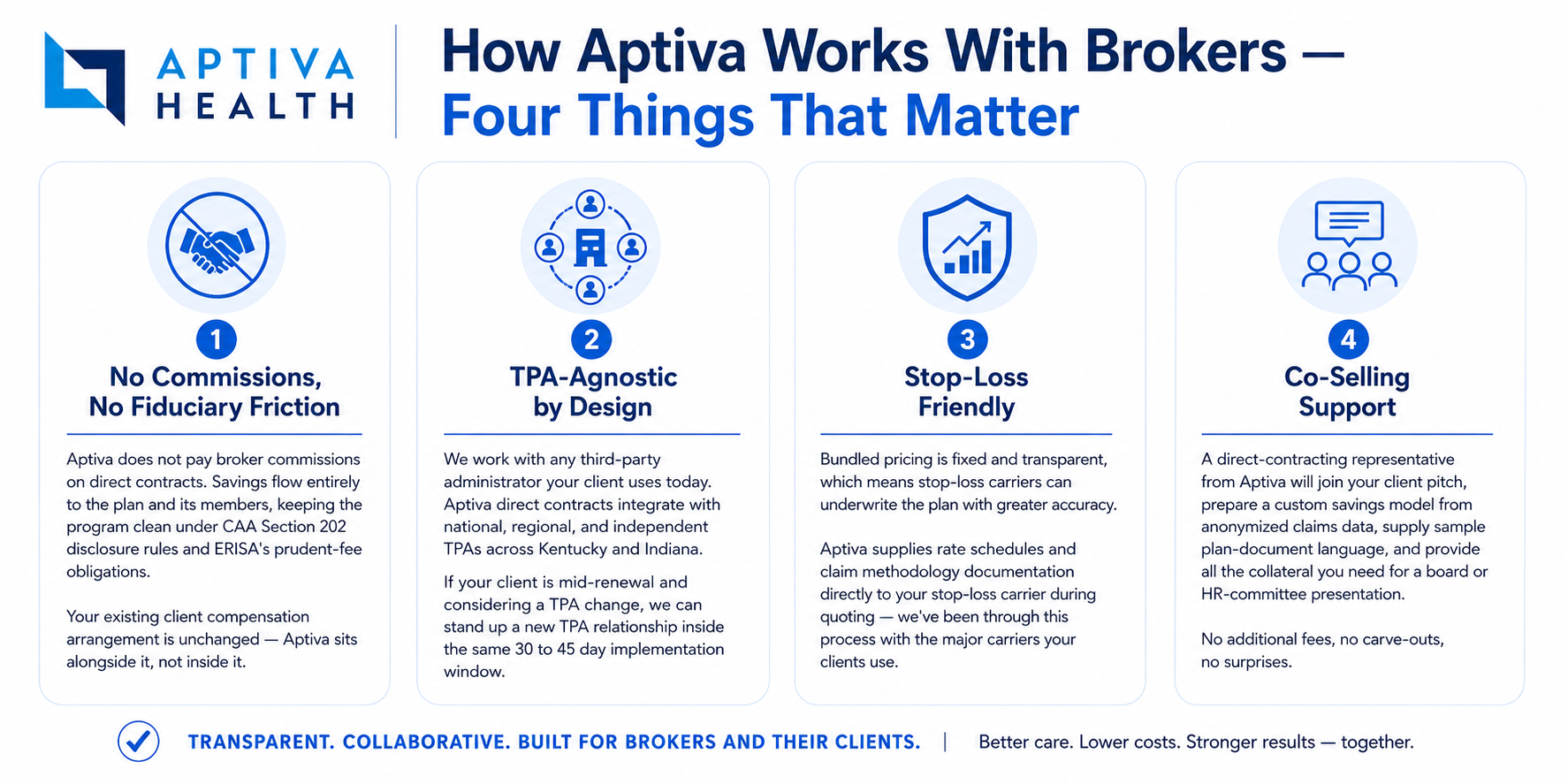

How Aptiva Works With Brokers — Four Things That Matter

1 · No Commissions, No Fiduciary Friction Aptiva does not pay broker commissions on direct contracts. Savings flow entirely to the plan and its members, keeping the program clean under CAA Section 202 disclosure rules and ERISA's prudent-fee obligations. Your existing client compensation arrangement is unchanged — Aptiva sits alongside it, not inside it.

2 · TPA-Agnostic by Design We work with any third-party administrator your client uses today. Aptiva direct contracts integrate with national, regional, and independent TPAs across Kentucky and Indiana. If your client is mid-renewal and considering a TPA change, we can stand up a new TPA relationship inside the same 30 to 45 day implementation window.

3 · Stop-Loss Friendly Bundled pricing is fixed and transparent, which means stop-loss carriers can underwrite the plan with greater accuracy. Aptiva supplies rate schedules and claim methodology documentation directly to your stop-loss carrier during quoting — we've been through this process with the major carriers your clients use.

4 · Co-Selling Support A direct-contracting representative from Aptiva will join your client pitch, prepare a custom savings model from anonymized claims data, supply sample plan-document language, and provide all the collateral you need for a board or HR-committee presentation. No additional fees, no carve-outs, no surprises.

Service Lines in Scope

A direct contract gives your client's plan access to Aptiva Health's full multi-specialty footprint across Kentucky and Indiana. In-scope service lines include:

Orthopedic Surgery — total joint replacement, sports medicine procedures, fracture care, hand and foot

Spine Care — cervical and lumbar disc replacement, microdiscectomy, SI joint fusion, minimally invasive fusion

Interventional Pain Management — epidural steroid injections, radiofrequency ablation, joint injections

MRI & Diagnostic Imaging — MRI in Louisville, Lexington, and Northern Kentucky with digital x-ray at each clinic location.

Physical Therapy — direct-access PT, one-on-one treatment time, in-house at every Aptiva location

Sports Medicine — non-operative and operative care, return-to-play and return-to-work pathways

Concussion Care — led by Dr. Lisa Manderino at the Aptiva Concussion & Sports Medicine Institute

Immediate Injury Care — same-day evaluation for sprains, strains, fractures, lacerations, and work injuries

Geography: 14 locations across Louisville, Lexington, Elizabethtown, Mt. Washington, Hebron (Northern KY / Greater Cincinnati), and Indianapolis. Map of every location at Locations.

Excluded from direct contract scope: Workers' compensation claims and auto / PIP injury claims. An Aptiva practitioner still coordinates care across those pathways so member experience remains consistent across the claim type.

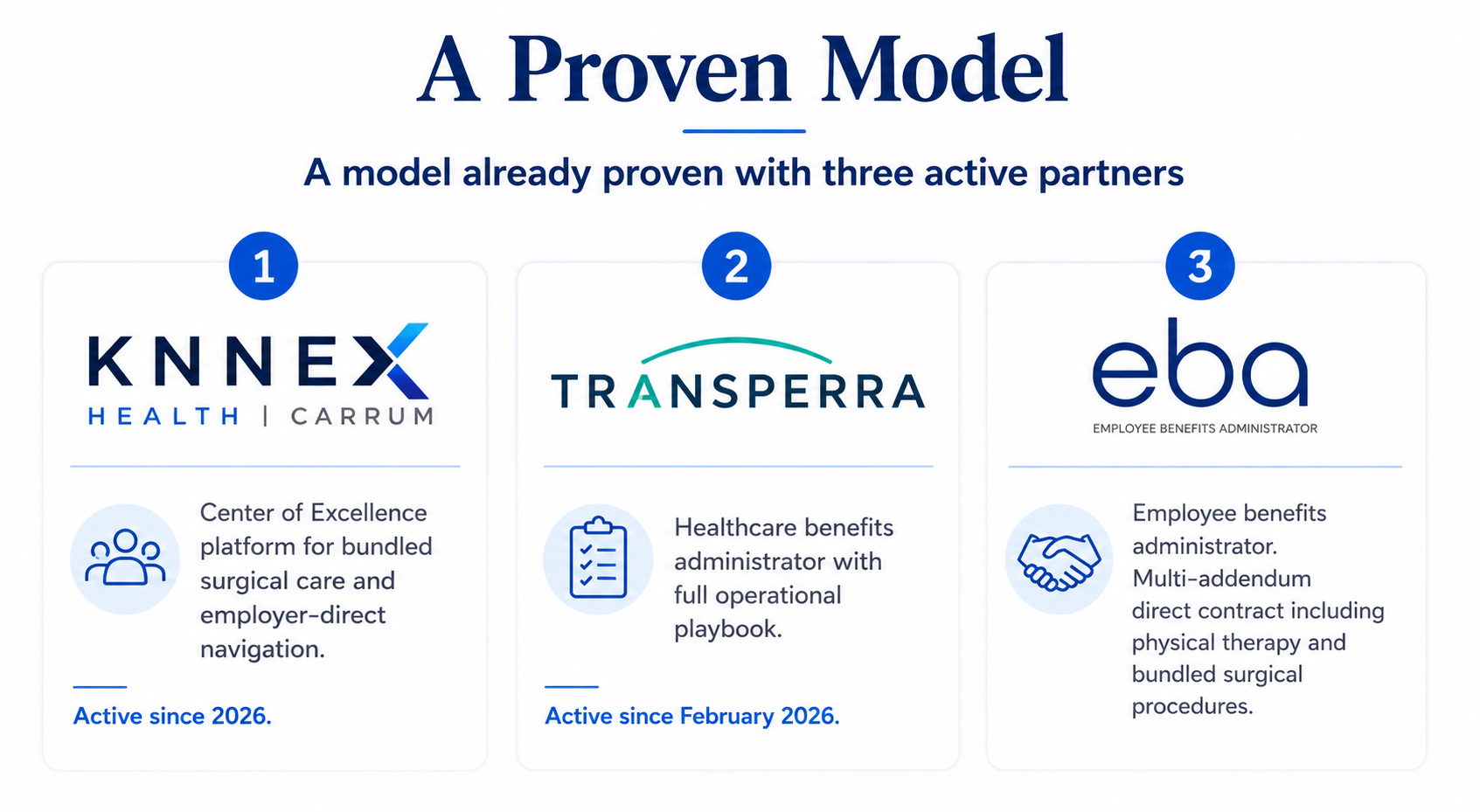

A Proven Model Across Kentucky and Indiana

{kind=link}

Aptiva Health has been delivering direct-contract care to self-funded employer plans across Kentucky and Indiana since 2025. Current partners include employers across manufacturing, transportation, professional services, and public-sector groups, with total covered lives in the hundreds of thousands. Quarterly savings reporting is provided to every broker partner so the renewal conversation is grounded in documented outcomes, not projected ones.

Frequently Asked Questions

How do brokers introduce Aptiva Health to a self-funded client? Start with a 20-minute discovery call between the broker, the client, and an Aptiva Health direct-contracting representative. Aptiva provides the savings model, sample plan-document language, and a custom rate exhibit. The broker remains the client's primary advisor throughout the engagement.

Does Aptiva Health pay broker commissions on direct contracts? Aptiva Health does not pay broker commissions on direct contracts. The savings flow entirely to the employer plan and its members, which keeps the program clean from a fiduciary standpoint under CAA Section 202 and ERISA's prudent-fee obligations. Brokers retain their existing compensation arrangement with the client.

Which TPAs and ASO administrators does Aptiva Health work with? Aptiva Health is TPA-agnostic. Our direct contracts work alongside any third-party administrator or ASO arrangement, including national, regional, and independent TPAs. We have active integrations with multiple TPAs across Kentucky and Indiana and can stand up a new TPA relationship in 30 to 45 days from agreement signature.

How does an Aptiva direct contract work with the client's stop-loss carrier? Aptiva direct contracts are stop-loss friendly. Because bundled pricing is fixed and transparent, stop-loss carriers can underwrite the plan with greater accuracy and often pass savings through in renewal pricing. We provide rate schedules and claim methodology documentation to support stop-loss disclosure during quoting.

What sales support does Aptiva Health provide to brokers? Aptiva supplies a full broker toolkit: program overview PDF, employer savings model, sample plan-document language, member experience materials, an editable savings chart for client presentations, and direct co-selling support from an Aptiva direct-contracting representative on client calls. Aptiva will join broker pitches at no cost.

Can a broker bring Aptiva Health to multiple clients at once? Yes. There is no exclusivity. Brokers can introduce Aptiva to every self-funded client in their book of business across Kentucky and Indiana. Each client gets a custom rate exhibit built for their specific claims profile and plan design, so contracts are not interchangeable but the broker-side workflow is consistent across groups.

Does using Aptiva Health protect a broker's renewal against a competing pitch? Direct contracting is one of the strongest renewal-defense tools available to brokers. Documented mid-year savings on surgical and orthopedic claims build a measurable case for plan performance at renewal, making it harder for a competing broker to dislodge an incumbent on price alone. Aptiva provides quarterly savings reporting brokers can present directly to clients.

What is the minimum group size for an Aptiva direct contract? There is no minimum group size. Aptiva's Direct Medical Services Agreement is structured to work for self-insured groups from a few hundred to several thousand covered lives, giving brokers a viable option across small, mid-market, and large self-funded books.

How long does it take from broker introduction to first eligible claim? Typical implementation is 30 to 45 days from agreement signature to first eligible claim. The full sequence — discovery call, savings model review, plan-document update, agreement signature, BAA execution, eligibility file share, go-live — usually runs 60 to 90 days from initial broker introduction to first eligible claim.

What is excluded from a broker-introduced Aptiva direct contract? Workers' compensation claims and auto/PIP injury claims are excluded from the direct contract — those are billed under separate Aptiva Health workers' comp and motor-vehicle accident pathways. An Aptiva practitioner still coordinates care across all three pathways so member experience remains consistent.

Add Aptiva Health to Your Client Conversations

Send a short note describing your book — number of self-funded clients in KY or IN, typical group size, and which renewals are open — and we'll set a 20-minute partnership call. No NDA required to talk; a mutual NDA is executed before any client-identifying data changes hands.

HIPAA notice: Do not include protected health information or client-identifying claims data in this form. Aptiva Health will execute a Business Associate Agreement before any PHI is exchanged.